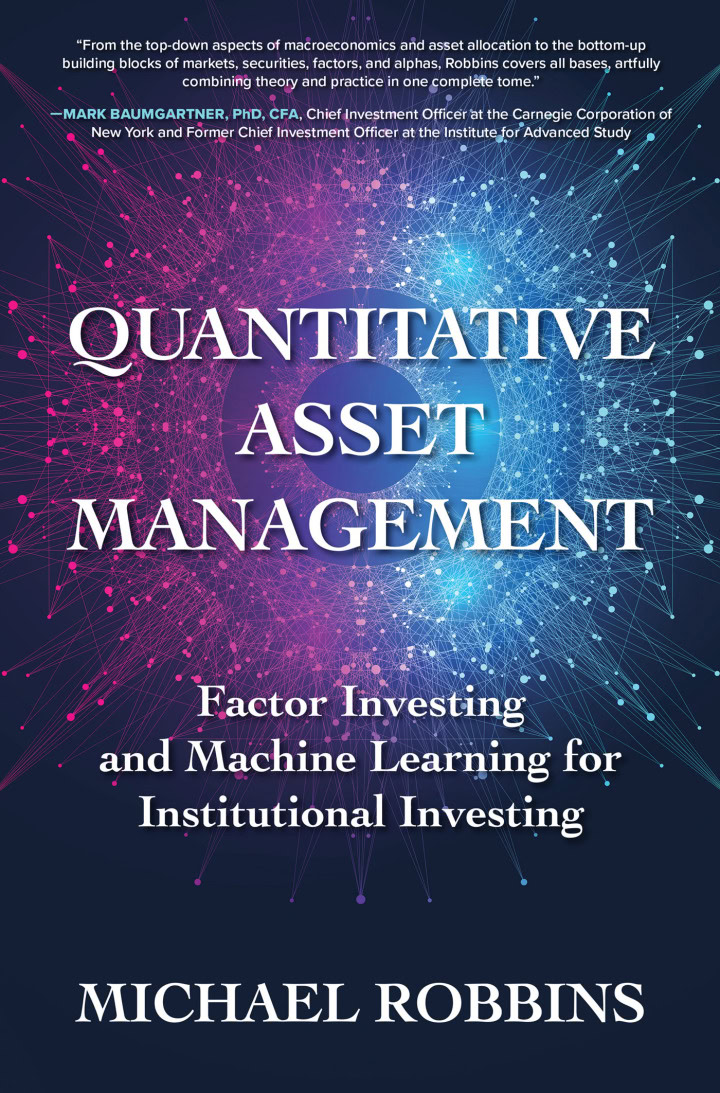

Whether you are managing institutional portfolios or private wealth, augment your asset allocation strategy with machine learning and factor investing for unprecedented returns and growth

Quantitative Asset Management (ePub) clearly illustrates the integration of factor investing with data science, specifically machine learning in the context of big data. This innovative guide, enriched with insightful anecdotes and practical examples—including quiz questions and a companion website featuring executable code—equips readers with essential tools to harness these cutting-edge techniques in their investment strategies. It thoughtfully addresses key real-world considerations, such as currency controls, market impact, and taxes. The book comprehensively guides readers through every phase of the investment journey, from goal-setting and planning to research, implementation, testing, and effective risk management. Inside, you’ll find:

- A toolkit for investing as a professional

- An accompanying online site with coding and apps

- Real-world investment processes as employed by the largest investment companies

- Clear explanations of how to use modern quantitative methods to analyze investing options

- Cutting-edge methods married to the actual strategies used by the most sophisticated institutions

Written by a seasoned financial investor who uses technology as a tool―as opposed to a technologist who invests―Quantitative Asset Management explains the author’s methods without oversimplification or confounding theory and math. Quantitative Asset Management demonstrates how leading institutions use Python and MATLAB to build alpha and risk engines, including optimal multi-factor models, contextual nonlinear models, multi-period portfolio implementation, and much more to manage multibillion-dollar portfolios.

Big data combined with machine learning provide amazing opportunities for institutional investors. This unmatched resource will get you up and running with a powerful new asset allocation strategy that benefits your clients, your organization, and your career.

978-1264258444, 978-1264258451

We highly recommend using the free Calibre to view the ePub ebook.

NOTE: This sale only consists of the eBook Quantitative Asset Management: Factor Investing and Machine Learning for Institutional Investing in the original ePub format. A converted PDF is available on request. No access codes are included.

Reviews

There are no reviews yet.